The scams that catch people off guard

A phone rings in the middle of the afternoon, and the caller already knows a name, a bank, or a bit of family detail. A text arrives saying there is a delivery problem, a tax issue, or an urgent payment to review. For many older adults, the hardest part is not spotting a strange message. It is deciding whether this one might be real.

That is exactly why Korea senior scams deserve serious attention. According to the Korean National Police Agency, voice phishing is one of the main fraud types causing major harm to older adults, with scammers pretending to be prosecutors, police officers, financial institutions, lenders, or even family members. The Financial Supervisory Service (FSS) has also warned that seniors in Korea can be targeted through illegal multi-level sales, fake investment-style schemes, misleading health supplement marketing, and so-called hyodo gwangwang (효도 관광, "filial piety" package tours marketed to seniors).

If you remember only one urgent step from this guide, remember this: if money has already been sent or account details were shared, contact the police at 112 or the FSS at 1332 immediately and ask about next steps, including payment suspension. That immediate reaction matters more than finding the perfect explanation.

For foreigners living in Korea, visiting with parents, or helping an older relative navigate Korean systems, the risk is not only fraud itself. It is also the extra pressure created by language barriers, unfamiliar institutions, and the assumption that a formal-sounding Korean message must be legitimate. That makes prevention much easier than recovery, so it helps to know what these scams usually look like before they happen.

Why seniors in Korea are often targeted

Most scams aimed at older adults are not technically complicated. They are emotionally precise.

Scammers look for moments when a person is likely to act first and verify later: fear about a child, respect for authority, concern about savings, anxiety about health, or embarrassment about "causing trouble." In Korea, where official institutions carry strong authority and many service interactions still happen by phone, fraudsters often build a script around that cultural familiarity.

For example, a caller may claim to be from the prosecution service, the police, a card company, or a bank security team. The call may sound formal, efficient, and urgent. The goal is to shut down normal skepticism and replace it with obedience. That is why older adults who are careful in daily life can still get caught by common scams in Korea.

The FSS has also highlighted scams that do not look like classic phone fraud at all. Some arrive as investment opportunities that promise safe returns. Some show up as health product seminars. Others present themselves as special tours, club memberships, or welfare-style benefits for seniors. In other words, elderly safety in Korea is not just about suspicious phone calls. It is also about recognizing when a polished sales pitch is actually a trap.

This matters for international readers because public English-language data on scams targeting foreign seniors specifically is still limited. But the core tactics are familiar enough that expats, long-stay visitors, and adult children helping parents in Korea should assume the risk is real, especially when stress and language confusion are added to the mix. Once you know the patterns, the warning signs become much easier to spot.

The main scam types older adults should know in Korea

Voice phishing and impersonation calls

This is the best-known category, and it stays dangerous because the scripts keep changing. The Korean police warn that scammers often pretend to be lenders, prosecutors, police officers, or financial institutions. Some say there is a legal problem. Some say an account has been compromised. Some say a loan can be approved only after a "temporary" transfer or identity check.

The details shift, but the structure is consistent: authority, urgency, secrecy, and payment.

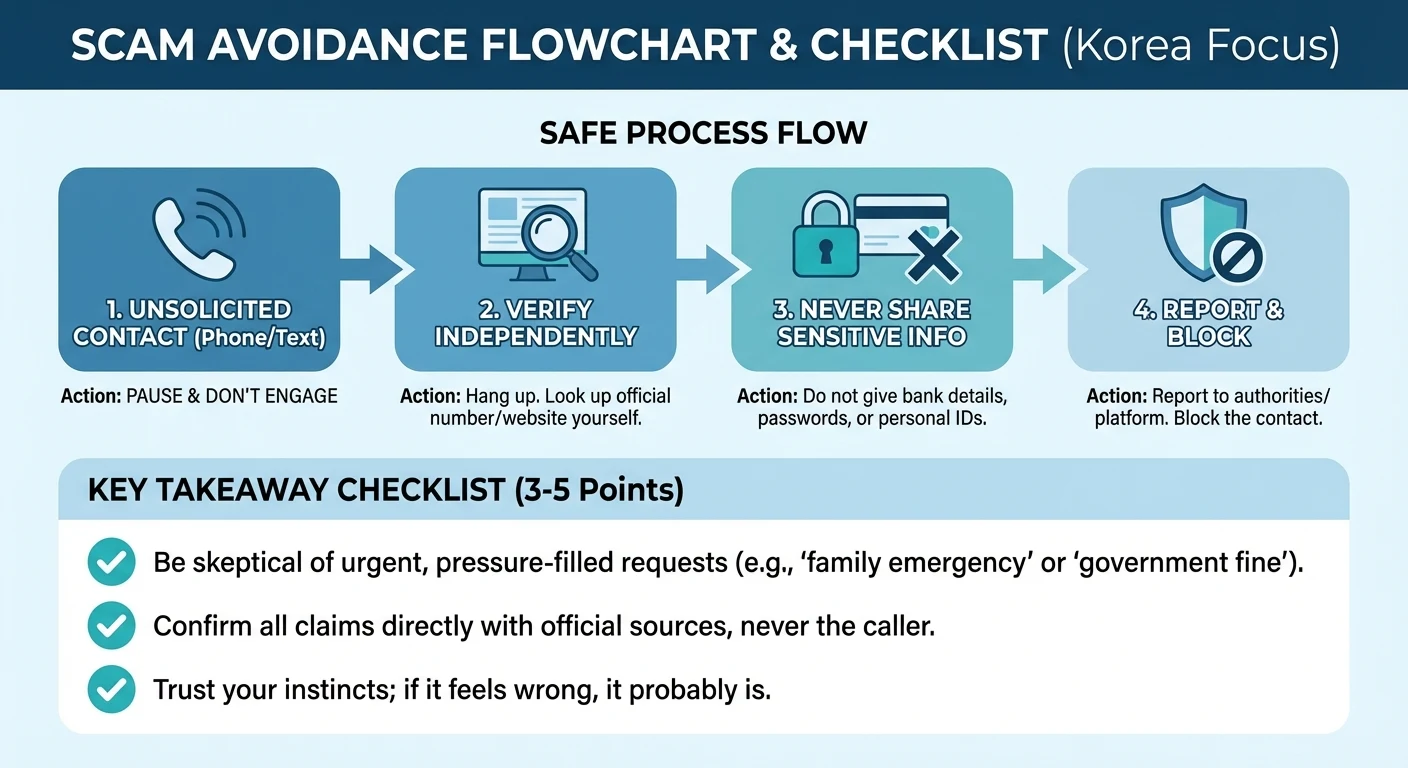

A scammer may say, "Do not tell anyone while this is being investigated," or "Transfer the money to keep your account safe," or "Install this app so we can verify your identity." That last part matters. The police specifically warn people to avoid installing apps from unclear or unofficial sources. In practice, this means never downloading an app because a caller or text message told you to.

For foreigners, the danger is straightforward: if the Korean side of the conversation sounds official, it can be tempting to cooperate first and translate later. That is the wrong order. Hang up first. Verify second. A real institution can survive a callback.

Family-emergency scams

Some fraud attempts use affection instead of authority. A caller or message may claim that a son, daughter, or grandchild is in trouble, has changed phone numbers, or needs money urgently. The police warn that impersonating a child or acquaintance remains a common method.

This can be especially effective with older parents whose children live abroad or travel frequently. Time zones, messaging apps, and changed numbers make the lie feel plausible. A senior in Korea may receive a message that sounds exactly like the kind of practical request a real family member would make.

The safest habit is simple: before sending money to a "family member," call that person directly using a number you already trust. Do not rely on the number inside the suspicious message itself. If they do not answer right away, call another relative or wait. Fraudsters push speed because delay helps the victim think clearly.

That same emotional pressure also appears in financial scams dressed up as opportunities.

Illegal investment and pseudo-deposit schemes

The FSS warns about yusa susin (유사수신, illegal pseudo-deposit schemes that present themselves like safe savings or investment products without legal authorization) as well as other fraudulent financial offers. These schemes often target seniors by promising stability, monthly returns, or "exclusive" access to something safer than ordinary markets.

The red flag here is not just a high return. It is the combination of high return, low risk, and social trust. The pitch may come through a church contact, a neighborhood introduction, a seminar, or a seemingly respectable office. Sometimes the scam uses Korean business language that sounds formal enough to disarm caution.

Older adults who have savings, retirement funds, or a lump-sum housing deposit may be seen as attractive targets. Foreign retirees or long-term residents can be vulnerable for an additional reason: they may assume a Korean-language brochure or office setup has already been vetted by authorities. It has not.

If someone says an offer is safe because "many seniors joined already," "this is not really an investment," or "the government knows about it," treat that as a reason to stop, not a reason to relax. A real financial product should be verifiable through official channels, and a legitimate adviser will not object when you take time to confirm.

The same logic applies when the scam is packaged as a wellness or consumer product instead of an investment.

Misleading health products and exaggerated wellness claims

One of the most emotionally difficult scam areas is health. The FSS has warned about false or exaggerated advertising involving health functional foods and related products. For older adults, these sales can be persuasive because they are often framed around fear, hope, and dignity rather than obvious greed.

A person may be invited to a lecture, a demonstration, or a trial session. The product may be described as special, imported, recommended for seniors, or only available for a limited time. It may not look like fraud in the classic criminal sense. It may look like pushy salesmanship. But when false claims, inflated pricing, or coercive payment tactics are involved, the financial harm can still be serious.

Not every supplement seminar is a scam. Not every wellness product is fake. The point is to separate ordinary marketing from danger signals. When the seller refuses to provide written details, rushes payment, discourages family consultation, or claims effects that sound medically dramatic, that is the moment to stop.

This is where many people realize that scams in Korea do not always arrive as obvious crime. Sometimes they arrive as "help."

Senior tours, seminar sales, and "special benefits"

The phrase hyodo gwangwang can sound warm and harmless because it draws on the idea of filial care for elders. But the FSS has warned that "filial piety" tour scams and similar sales approaches can exploit seniors' trust and social expectations.

These offers may begin with a low-cost or free trip, a gift event, or an information session. Once the group is gathered, the pressure starts: limited-time products, memberships, financial products, or health items. Seniors may feel social pressure not to be rude, not to appear suspicious, or not to "miss out" after already spending time there.

Foreign residents with older parents visiting Korea should pay attention to this category. A parent may say they are simply joining a local tour or lecture for fun, not realizing that the real purpose is high-pressure selling. A little curiosity beforehand can prevent a large payment later.

By this point, a pattern should be clear: the exact script changes, but the warning signs repeat.

Red flags that matter more than the story

You do not need to memorize every new scam type. In most cases, these warning signs are enough.

- Urgency: "Right now," "within minutes," or "before your account is frozen."

- Authority pressure: police, prosecutors, banks, card companies, or government offices demanding immediate action.

- Secrecy: being told not to tell family, bank staff, or friends.

- App installation: being told to install an app from a text link or unknown source.

- Transfer instructions: especially requests to send money to a personal account or through unusual channels.

- Identity harvesting: requests for resident registration details, account numbers, card information, passwords, or one-time authentication codes.

- Emotional leverage: a child in trouble, a grandchild with a new phone, or a "special" offer only for seniors.

- Pressure not to verify: irritation when you say you want to call back or ask family first.

A confusing call is not automatically fraud. A demand for secrecy, money, app installation, or fast identity confirmation is the line where you stop and verify. That makes the next step practical: building a routine that reduces panic in the moment.

A simple prevention routine for seniors in Korea

The best fraud prevention in Korea is not constant fear. It is a repeatable routine.

Use the "hang up, look up, call back" rule

If someone claims to be from a bank, police office, prosecutor's office, or government agency, hang up. Then find the official number yourself and call back. Do not use the number sent by text or spoken by the caller.

This one habit defeats a large share of phone-based scams.

Never install an app from a call or text

The Korean police specifically warn against installing apps from unclear sources. If a caller says the app is needed for identity verification, account protection, or investigation support, assume it is unsafe until proven otherwise.

A legitimate bank or public institution does not need you to comply with a stranger's instructions over the phone.

Verify family requests with a real voice call

If a message says your child or grandchild changed numbers and needs money, call the original number you already know. If needed, call another family member too. Do not continue the conversation only inside the suspicious chat.

For adult children of seniors, this is a good reason to create a family verification plan now, before anything happens.

Slow down all same-day financial decisions

If a sales pitch or investment offer demands payment today, that is already a problem. Wait one night. Ask someone else to look at it. Read the written material again. Scammers hate delay because calm thinking breaks the spell.

Create a "trusted contact" rule

If you are helping an older parent in Korea, agree on one rule: no transfer, no account sharing, and no contract signing without checking with one trusted person first. It can be a child, spouse, sibling, neighbor, or social worker. The main value is not expertise. It is interruption.

Keep emergency numbers visible

A small card near the phone can help. Include:

- `112` for police

- `1332` for financial fraud or financial consumer help

- A bank's official customer service number

- One family contact

- `1330` for multilingual travel help if language support is needed

This may sound basic, but during a stressful call, basic is exactly what works.

Once prevention fails, speed matters more than pride.

What to do immediately if you think a scam has happened

1. Stop the conversation

Hang up. Stop replying. Do not argue and do not try to "win" the conversation. Scammers are trained to keep people emotionally engaged.

2. Contact your bank right away

If money was transferred, card details were shared, or suspicious banking activity appeared, call your bank immediately. Ask about freezing transactions or other emergency fraud procedures.

3. Report to the police or FSS without delay

In Korea, the practical first contacts are:

- 112 for the police

- 1332 for the Financial Supervisory Service

The police and FSS both emphasize fast reporting when fraud occurs, especially if payment suspension may still be possible.

4. Get language help if needed

If the person affected cannot explain the problem comfortably in Korean, use the 1330 Korea Travel Helpline from the Korea Tourism Organization for multilingual assistance. It is not a fraud investigation line, but it can help bridge the language gap and point travelers toward the right service.

5. Save evidence

Keep screenshots, call logs, bank transfer records, names used by the scammer, account numbers, websites, and any app links received. Do not delete the messages out of embarrassment.

6. Treat shame as irrelevant

Many older adults delay reporting because they feel foolish or worry about burdening family. That delay helps the scammer, not the victim. The right standard is not "I should have known better." The right standard is "I am acting quickly now."

For foreigners who leave Korea soon after the incident, official guidance is much stronger on immediate reporting inside Korea than on follow-up once someone is back overseas. If that situation applies, report while still in Korea if possible, contact your bank immediately, and keep all records for local police or consular follow-up later.

Extra advice for expats, travelers, and families

If you are an expat with visiting parents, do not assume Korea will feel obviously risky to them. In fact, the opposite can happen. Korea often feels organized, digital, and efficient, which can make a scammer's script sound more believable.

A few practical steps help a lot.

If your parent is visiting Korea

Tell them in advance that police, banks, and government agencies do not call to demand instant transfers. Also tell them not to trust texts about customs fees, account problems, or delivery issues unless they verify independently.

If your parent lives in Korea

Set up a routine check-in about unusual calls, not just emergencies. Many people mention suspicious calls only after they lose money because they do not want to sound alarmist.

If language is a barrier

Put key phrases and numbers in both English and Korean on paper. Even a simple note can help:

- "Please hang up and call me first."

- "Do not install apps from text messages."

- "Call 112 if pressured."

- "Call the bank's official number only."

If a scam looks like a consumer dispute

For problems involving deceptive sales, product pressure, tours, or other consumer issues, the Korea Consumer Agency can be useful for foreigners through its counseling contact. It is not a replacement for police reporting when money is at immediate risk, but it can help when the issue overlaps with consumer harm rather than pure phone fraud.

That is an important distinction. Some cases are clearly criminal. Others sit in the uncomfortable space between fraud, misrepresentation, and aggressive selling. Either way, early advice is better than late regret.

Official resources in Korea

If you want one section to bookmark, make it this one.

https://www.police.go.kr/www/security/fraud/fraud03.jsp

- Korean National Police Agency: voice phishing prevention information and reporting guidance

https://ecrm.police.go.kr/minwon/main

- Police cybercrime reporting system (ECRM): online reporting and consultation

https://www.fss.or.kr/

- Financial Supervisory Service (FSS): financial consumer protection information and fraud response support via `1332`

https://english.visitkorea.or.kr/ https://english.visitkorea.or.kr/svc/contents/infoHtmlView.do?vcontsId=140042

- Korea Tourism Organization: `1330` Korea Travel Helpline for multilingual help

https://www.kca.go.kr/eng/ https://www.kca.go.kr/eng/sub.do?menukey=6014

- Korea Consumer Agency: foreigner consumer counseling

The bottom line

Protecting older adults from scams in Korea is less about learning a perfect list of bad actors and more about learning a few non-negotiable rules. Hang up, verify independently, never install unknown apps, never transfer money under pressure, and report quickly if something has already gone wrong.

The most important thing to understand is that these scams work because they are designed to feel believable in the moment. That is why calm routines matter so much. For seniors, families, expats, and travelers alike, the safest approach is not paranoia. It is having a plan before the next convincing call arrives.